Speeding along with Tesla

Tesla Inc is the sixth largest company in the world by market capitalisation (Source: Refinitiv as at 17 Nov 2021). Of the top ten largest companies in the world Tesla is the most volatile with a one year historic volatility of approximately 56%. This is more than 10 percentage points higher than the next highest in the group (Tencent Holdings Ltd at approximately 42%). This company has demonstrated strong price growth and with its high volatility has appeal to retail and institutional investors through direct or option based investments.

Presence in structured products

Tesla is a popular structured product underlying and is ranked eighth in the US by product issuance in 2021 to date and is the top stock by the same measure. By sales volume Tesla accounts for 1.38% of the market share which makes it the second highest stock underlying behind Apple with 1.49%. Source for this data is www.structuredretailproducts.com. The most common payoffs linked to Tesla are the Reverse Convertible and Knock Out. Both are “at-risk” strategies that will be able to offer high returns when linked to a volatile underlying. Most Tesla products have a maturity of between one and three years. In addition to Tesla only linked products it also features in multi-asset products with a worst-of payoff.

A recent example of a typical Tesla product is a 18 month phoenix auto-call product issued by JP Morgan paying monthly coupons equivalent to 12.35% per annum as long as the underlying is greater than 60% of its initial level. The product will call if the underlying is at least equal to its initial level on any quarterly measurement date. Capital is at risk at maturity if the underlying finishes below the 60% barrier.

The strike date of this product is 1 November 2021. The level of the stock on this date was 1208.59 and therefore the barrier level for this product is set at 725.15. The last time the share price was below the barrier level was 27 Aug 2021, barely two months before the strike date of the product. The one year implied volatility of the stock is currently around 58%. The implied volatility and the recent moves in the share price should remind investors that although a 60% barrier provides some protection it has to be considered in the context of the underlying and its high volatility. As with most auto-call products the most likely outcome under option pricing models is that the product will call on the first date and pay the relevant coupon providing the investor with a decent income stream (albeit for only a short period).

Strong growth, high volatility

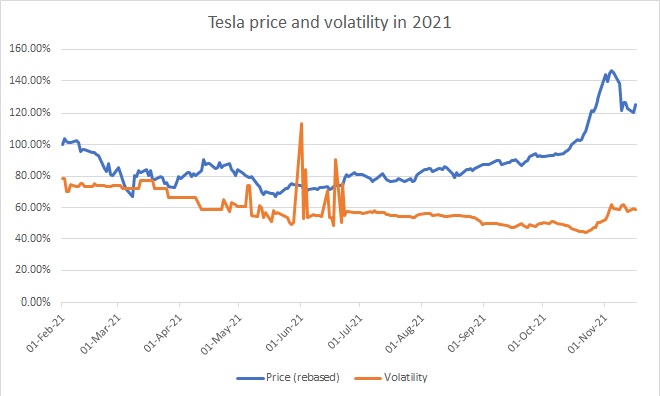

Fig 1: One year implied volatility and the rebased performance of Tesla Inc from 01 Feb 2021

The chart shows the rebased level of the stock and the one-year implied volatility from the beginning of Feb 2021. This chart shows that although still volatile compared to other similarly sized companies the implied volatility has fallen throughout the year. The most volatile period this year was in June which coincided with news of supply chain issues and delays in production. The last couple of weeks has seen a fall in share price and a corresponding increase in volatility.

Top of Performance tables

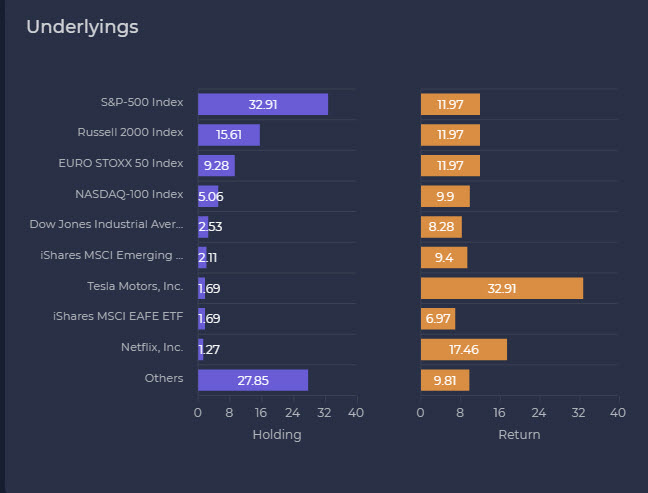

Fig 2: US market representative sample of live structured products showing proportion and annualised returns (Source: SRP/FVC structured product lifecycle application as at 29 Oct 2021)

Output from the SRP/FVC structured product lifecycle application in Figure 2 gives a snapshot of structured product returns for a representative sample of US products. Whilst Tesla is a relatively small proportion of the holdings the annualised returns of Tesla based on product maturities and live valuations hugely outperform the other major underlyings. The products linked to Tesla are mostly Autocalls, Phoenix Autocalls or Reverse Convertibles which don’t require underlying growth to generate returns. Instead they pay coupons or auto-call payments which will be relatively high given the stock’s volatility level. The recent growth in the underlying will increase the chance of a positive return.

This strong performance is derived from retail structured products issued on the back of investor demand and market opportunity. It will also attract interest from institutional investors, quantitative funds and hedge funds who can use market timing to bet on direction and to take advantage of volatility levels. These can be achieved by direct trading of stock and listed options or through bespoke derivatives traded with an investment bank. While institutional investors have the ability to strike more complex and tactical deals in essence they are similar to the ones available in the retail market that have shown such high returns.

Tesla is a significant global company and very important in the structured product market. It is a volatile and exciting stock which is frequently present in traditional and social media. The recent news of JPMorgan pursuing legal action against them being the latest story. However regardless of short term falls or negative press the stock continues to provide investors with very attractive returns through both growth and volatility plays.

Tags: InvestmentA version of this article has also appeared on www.structuredretailproducts.com

Image courtesy of: Aditya Chinchure / unsplash.com