An Introduction to Autocallable ETFs

Autocallable notes continue to dominate the structured product market, with structured product issuance exceeding USD195 bn in the US in 2025 and autocalls equating for over 43% of the whole market. In 2025, this momentum led to the launch of a new autocallable ETF format.

Growth of Autocallable Structures

Structured notes and ETFs traditionally have some fundamental differences, namely that an ETF is a pooled investment holding a basket of assets whereas a structured note is issued by a financial institution and often has a non-liner payoff linked to an index or other asset. ETF returns move directly with the value of their holdings whilst structured products are a buy-to-hold investment with additional credit risk. The challenge when creating a structured ETF is to keep the benefits of an ETF such as liquidity and transparency whilst incorporating autocall payoff features.

Although the concept of an autocall ETF is a relatively new one there have been structured product mutual funds available for much longer. One of the largest and most well-known is the Atlantic House Defined Returns Fund in the UK market. This fund holds a portfolio of autocall swaps linked to global equity indices. It currently has GBP 2.66bn under management and has delivered steady, low-volatility growth, with an annualised growth of 7.3% over the past five years.

The First Autocallable ETF: Calamos Leads

Calamos has emerged as the early leader in bringing structured note characteristics into the ETF world, carving out a new category with its autocallable strategies. The firm introduced the Calamos Autocallable Income ETF (CAIE) in June 2025, the first autocallable structure packaged inside an ETF. CAIE is built around a laddered portfolio of more than 50 autocallable notes. The autocalls themselves are linked to the MerQube US Large Cap Vol Advantage Index a volatility controlled decrement index that tracks the performance of E-Mini S&P 500 Futures Contracts. Each note in the portfolio has the same structure, it has a five-year maturity and a monthly income stream which is paid if the index is great than the income barrier of 60% of the starting level allowing the fund to generate a high monthly income as long as the index does not fall by more than 40%. The products will call if the index is above its starting level on an autocall date. J.P. Morgan is the counterparty although as the trades are swaps there is not the same level of counterparty risk as for traditional structured notes. As of the end of April 2026 there were 61 autocalls in the portfolio with an average coupon of 14.02%. All of the live trades paid coupons at the last opportunity. The ETF itself has an annual distribution rate of 14.3% based on its first year of trading.

New Entrants and Variations

The strong reception for the CAIE, as highlighted by surpassing USD 870 m AUM has encouraged other asset managers to enter the space, and the competitive landscape has grown rapidly. Since mid-2025, more than 10 rival autocallable ETFs have launched. Firms such as First Trust, Innovator, TrueShares and REX Shares have introduced their own interpretations of the structure. TrueShares has a similar approach to Calamos but rather than fixing the trade terms they have a target income level and will vary the product terms i.e. coupon barrier, maturity and maturity barrier to achieve the target income level. This will lead to a greater variety of product structures in the portfolio. GraniteShares has taken a more specialised approach by launching the first single-stock autocallable ETFs, offering concentrated exposure to companies such as Tesla and Nvidia through diversified note portfolios. The result is a fast-expanding ecosystem that reflects how quickly the market has embraced this new concept.

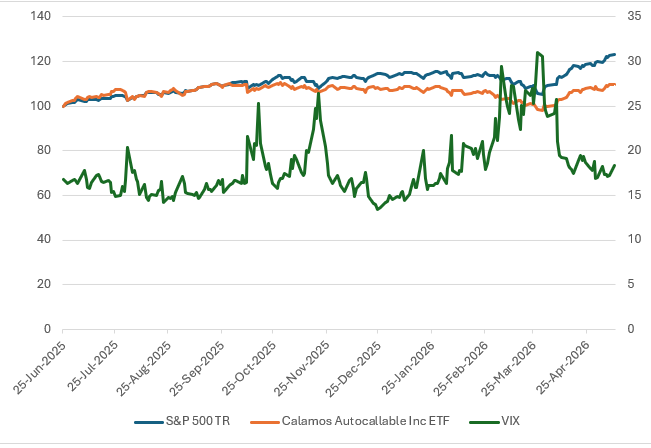

This chart highlights the divergence between the Calamos Autocallable Income ETF and the underlying S&P 500 over the period shown. While the S&P 500 Total Return index rose steadily to around 123% of its starting level over the period, the ETF lagged materially, finishing closer to 110%. Although the ETF broadly tracked the direction of the equity market, it did not capture the full upside of the index. The difference in the growth of the two underlyings is explained by the income paying nature of the structures held within the ETF. The fund has paid approximately 14% in income over the past year which when combined with the growth slightly exceeds the S&P total return.

Both the Calamos Autocallable Income ETF and the S&P 500 show declines during spikes in the CBOE Volatility Index, particularly during the larger volatility events in late 2025 and early 2026. This is consistent with typical equity market behaviour, where periods of market weakness and rising volatility tend to occur together.

Autocallable ETFs have quickly established themselves as a new addition of a structured-payoff design as opposed to being an extension of the structured-note market. Their early adoption led by the CAIE shows that investors are interested in accessing defined income payouts and barriers-based outcomes through a transparent, ETF format. This structure allows investors to access autocallable type outcomes through an ETF vehicle on an ongoing basis without some of the perceived weaknesses of traditional structured notes.

This article was generated from data coming from the SRP Greeks application, a service which provides aggregate Greeks data on important underlyings in structured product markets. The product set is taken from the SRP database and all calculations and analytics are powered by FVC. For more information contact www.structuredretailproducts.com.

Tags: Product typesImage courtesy of: Pawel Czerwinski / unsplash.com