Eurostoxx 50 and SMI: An Exposure Comparison

The Eurostoxx 50 and Swiss Market Index (SMI) represent two major European markets, making it valuable to analyse their impact on structured products, since both indices are popular underlyings. The Eurostoxx 50 represents the largest companies in the Eurozone and has a total capitalisation of around EUR 4 Tn. This index includes ASML (semi-conductors), LVMH and L’Oreal. The SMI features Roche, Novartis and Nestle and other large cap Swiss companies.

Performance and Sector Comparison

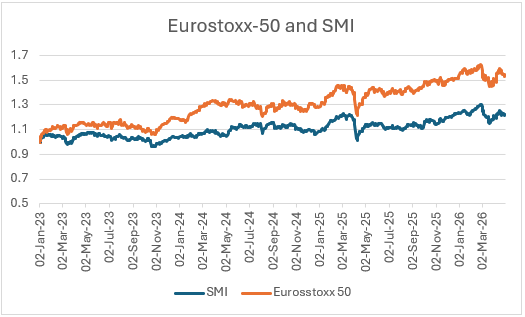

In the 12 months to the end of April 2026, the Eurostoxx 50 has risen around 11% whereas the SMI has only risen by about 7%. On a three-year view (since January 2023) their performances have been +55% and +22% respectively. This performance reflects the sectors that make up each index. The Eurostoxx 50 is well diversified and includes many technology firms including ASML, whereas the SMI is more concentrated on healthcare, retail and financials.

Notional and Usage Trends

SRP Greeks data (source: www.structuredretailproducts.com) at the end of April 2026 shows the Eurostoxx 50 has the third highest notional of all underlyings, behind only the S&P-500 and Russell 2000, making it a very important index for structured products Greeks exposures. The SMI is the eighth highest underlying but with a much smaller share since these top three indices dominate the data set. The Eurostoxx 50 has around 16.6% share of total notional compared to the SMI at only 1.1%. We can contrast this with the total activity by region, which is much more even, Eurozone coming in at about 12.2% of market share and Switzerland at 9.8%.

Both Eurozone and Switzerland have very active structured products markets, but very little of either is linked to the SMI because Switzerland overall has a small economy. Furthermore, the Eurostoxx 50 and SMI are heavily used outside Eurozone, with it being particularly popular in the US market. The major difference is that the Eurostoxx 50 is often used as a single underlying and it is by far the most popular choice in the US of all non US underlyings. In contrast, the SMI generally appears as part of a basket. For Eurostoxx 50 linked products the total notional of products on the database is around USD 43 bn, but when accounting for other underlyings the proportion that can be attributed to the Eurostoxx is 71%, indicated a high proportion of single underlying products. For the SMI, overall notional is much lower at USD 7 bn and the attributed proportion is only 33%.

For example, the highest notional product linked to the Eurostoxx 50 is a single underlying Autocallable issued in the USA. The largest product linked to the SMI is made up of a basket of SMI, FTSE-100 and Eurostoxx 50.

Greeks and Underlying Structure

The overall Greeks sensitivities show some contrasts between the two indices, even accounting for size differences. The first is that the relative delta, a measure of delta as a proportion of the notional amount stands at 46% average for Eurostoxx 50 products and only 22% for SMI linked products.

This is a fundamental difference and is due to either product differences or recent index performances. The main reason is because many more Eurostoxx linked products are single underlyings only and not as part of a basket. In A product’s overall delta is split across each underyings depending on which one is likely to contribute more to the final payoff. Additionally, more Eurostoxx products are Growth types which tend to have higher delta.

Gamma is around ten times higher on a relative basis for the Eurostoxx-50 products and Vega around four times higher. Both are consistent with the behaviour of Growth products and the effect of the Eurostoxx being the sole underlying in more products.

Fully analysing the Greeks exposures from a set of structured products is done by product valuation, sensitivities, and aggregation across all products on the database. However, an important factor is the number of underlyings in the product set. Generally, in the structured products market there are individually linked products as well as those that use basket or worst-of constructions. Furthermore, it tends to be true that important global benchmark indices along with popular single stocks have a higher proportion of single underlying products. This means the exposure for these underlyings comes through more strongly and that the exposure will directly depend on them and not be influenced by the movement of other underlyings that will affect the basket performance. Aggregating global Greeks exposures can depend on many factors but in this case the dominant cause is the simple explanation of the underlyings make-up.

This article was generated from data coming from the SRP Greeks application, a service which provides aggregate Greeks data on important underlyings in structured product markets. The product set is taken from the SRP database and all calculations and analytics are powered by FVC. For more information contact www.structuredretailproducts.com.

Tags: Product typesImage courtesy of: Ricardo Gomez Angel / unsplash.com