Testing times at Netflix

The US TV and film streaming company Netflix is the latest high-profile name to experience difficulties in the stockmarket. Its stellar growth in the last few years and high visibility gave it frequent coverage in the financial press. In common with other darling stocks such as Tesla and GameStop it resonated with ordinary investors and was not dependent on the institutional sector to propel it into the limelight.

Astonishing growth and subsequent troubles

The main growth period of Netflix started from the beginning of 2020 with the stock at USD 330. It reached a high of USD 680 in November 2021. Therefore, in less than two years the stock had more than doubled in price compared to a rise in the S&P-500 of less than 50% (which itself represented very strong growth). Netflix was perceived to have been one of the main beneficiaries of the change of working and social habits during the pandemic. This put it in the category of strong performing companies such as Zoom which posted standout gains as a resulted of blanket news coverage and strong interest and increased revenue before falling back after it lost momentum.

A strong increase in the number of Netflix subscribers led to greater earnings and rapidly increasing market P/E ratings which propelled the stock to such heights. The main rationale was that in the virtual and budget conscious world that consumers now found themselves in low cost technology based solutions were a clear winner. However, from the end of 2021 the picture for Netflix changed quite suddenly as can often happen in such investment bubble scenarios. As lockdowns ended around the world and Netflix had arguably reached near realistic saturation levels the momentum of subscriptions shifted somewhat towards decline. This was enough to cast doubt on the stock price which then fell very rapidly. Netflix stock is now currently trading at around USD 180, representing a fall of nearly 75% from the peak.

Structured product usage

With its high volatility, strong growth story and brand name in the market it is not surprising that Netflix has proven a popular underlying for structured products in the last few years. Data for www.structuredretailproducts.com shows that there are around 1250 live products linked to Netflix. Not surprisingly, the biggest market is the US with over 500 products and a total of USD 1.2 bn notional. This is to be expected given the strong structured product market in the US and the fact that Netflix is an American company. Other markets with sizeable issuance in Netflix linked products include Spain, Switzerland, Italy, Taiwan and South Korea.

Issuance by product type and characteristics is also interesting. Over half of the Netflix linked products are yield generating worst-of structures. Popular choices to go alongside Netflix are Walt Disney, Amazon, Microsoft, Apple, Alphabet, Meta and Oracle. These products therefore have a technology and entertainment theme, with Netflix arguably sitting in both categories.

Whether the product is Netflix linked only or structured as a worst-of, the most common product types are Reverse Convertibles, Income and Snowball Auto-calls and Callables. These are the most popular yield generating products in markets worldwide and make a lot of sense for an underlying such as Netflix. A stock that has risen significantly and that has a high volatility (its one-year implied volatility is now around 50%) is perfect for a yield generating product because of the high yield that can be easily offered and the relatively deep barrier level that can be afforded. In many cases the barrier level can be set at 50% or 60% of the initial stock level.

While many investors would not expect Netflix to return to the levels seen six months ago, most would probably trust the stock to be able to comfortably stay clear of the dollar level implied by a deep barrier. A 60% barrier from a strike price of USD 180 is down at USD 108, meaning that no capital would be lost unless Netflix fell below this level, which the stock has not been at since the end of 2016.

Analysing Netflix products

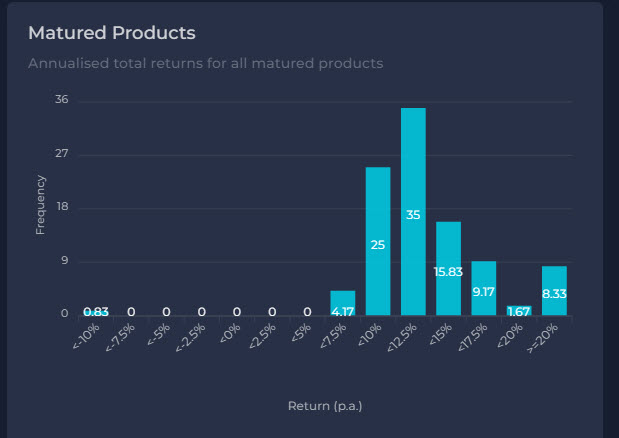

Data from Structpro.com gives an interesting breakdown of recent Netflix linked products, both live and matured. The first point to note is that of the 264 products that have already matured, only one showed a loss. This was a leveraged return product with a relatively high barrier (75%) and matured with the underlying at 71% of its start level. Much more typical however is the worst of Netflix, Amazon and Meta Income Autocall with a 32% p.a. annual income which successfully called after one year. The average annualised return is nearly 25% p.a.. The income Autocall is in fact the most dominant product type accounting for over 95% of all Netflix products. The five biggest issuers of Netflix linked products are UBS, Citi, Credit Suisse, Morgan Stanley and Goldman Sachs.

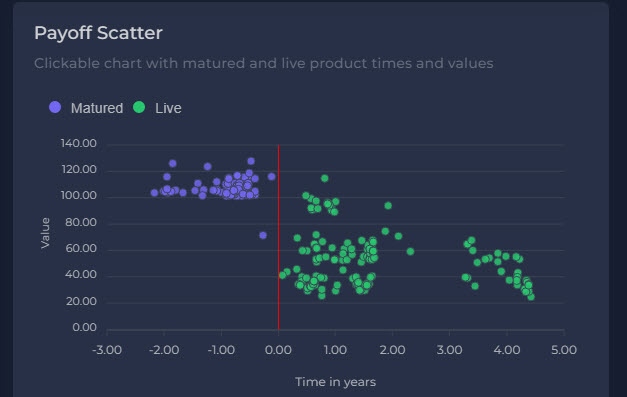

The picture when analysing live products is rather different. The Structrpro platform makes it very easy to compare results for different portfolios and product sets. Due to the types of products linked to this underlying and the recent decline in the stock price most products that are still live will have suffered mark to market losses. All products except three are currently sitting on a mark to market loss. The average barrier (and contingent coupon) level across all live Netflix products is 62% as measured at inception (typically in the range 50%-75%) but relative to today’s market level it stands at 180%. This means that the average product is significantly below its barrier level and is therefore headed for capital loss unless the stock recovers. Similarly, the picture for Auto-calling is as bleak, with the average level required to successfully call being 300% of the current stock level.

It hardly seems possible that such a huge discrepancy between matured and live products can exist, but this is due to a combination of the relatively short maturity of products and the extreme stock price moves that have been seen. Monitoring a client’s portfolio in detail is an important exercise in both strong and weak market conditions and this is made easier than ever before with Structrpro.com.

Tags: LifecycleA version of this article has also appeared on www.structuredretailproducts.com

Image courtesy of: Venti Views / unsplash.com