Navigating structured products in France

An in-depth look at any financial market over 2020 would undoubtably produce some interesting analysis. When looking back on volatile periods we can see the strengths and weaknesses of particular investment types and this provides good insight into how they might fare in extreme conditions.

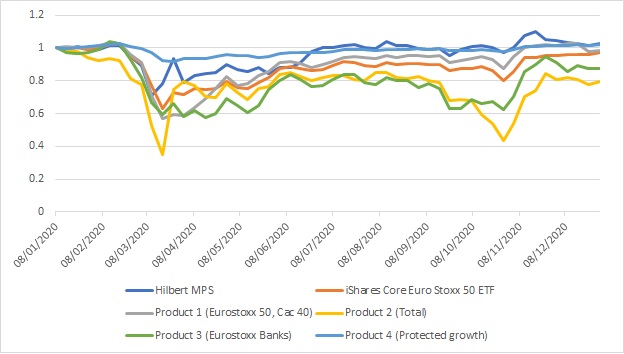

This piece is going to consider the French market during 2020 with a focus on how four structured products performed over the year. For comparison we will also consider the Managed Portfolio Service (MPS) from the structured product provider Hilbert. Styled the Hilbert Rendement Life, it aims to generate on average 8% per annum through investing in a portfolio of phoenix autocall structured products. The products are generally capital at risk with a barrier of 60% and are linked to major equity indices.

The individual structured products chosen for this analysis comparison all had strike dates towards the end of 2019 and were live throughout the entire twelve months of 2020. These products are all linked to underlyings popular in France. The Eurostoxx 50 index was the largest index by sales volume in 2020 and the French national index the CAC 40 was the most common underlying by number of products issued during this year (data from www.structuredretailproducts.com). All four of the products plus the MPS have autocall features which are extremely popular in France (as they are globally). Three of the products are at risk phoenix autocalls offering conditional income based on the performance of the underlying and Product 4 is a 95% capital protected product with a single autocall opportunity half way through the product term. If the autocall is not triggered the product will pay a return dependent on the growth of the underlying at maturity. The level of the index used to calculated the performance is the average of index values taken every six months throughout the product term.

The product terms were all sourced from www.structuredretailproducts.com, and the independent fair values for this analysis are calculated by FVC’s Nextval valuation platform at www.futurevc.co.uk/nextval.

| Issuer | Product type | Strike date | |

| 1 | Hilbert | Managed Portfolio Service | Open Ended |

| 2 | Societe Generale | Pheonix Autocall | 43819 |

| 3 | BNP Paribas | Pheonix Autocall | 43812 |

| 4 | Credit Suisse | Pheonix Autocall | 43798 |

| 5 | Amundi | Protected growth | 43826 |

The chart below shows the performance during 2020 of the four structured products, the managed portfolio and the iShares Core Euro Stoxx 50 ETF (as an equity benchmark). The price series of all the instruments have been rebased to 100% at the start of the year. The table shows a set of summary statistics for the same set of instruments.

| Instrument | Historical volatility | Return in 2020 | Sharpe ratio |

| Hilbert MPS | 0.415 | 0.027 | 0.064 |

| iShares Core Euro Stoxx 50 UCITS ETF EUR (Acc) | 0.38 | -0.03 | -0.08 |

| Product 1 (Eurostoxx 50, CAC 40) | 0.438 | -0.018 | -0.042 |

| Product 2 (Total) | 1.127 | -0.204 | -0.181 |

| Product 3 (Eurostoxx Banks) | 0.573 | -0.125 | -0.218 |

| Product 4 (Eurostoxx 50 - Protected growth) | 0.081 | 0.019 | 0.233 |

The instrument with the highest Sharpe ratio is the principal protected structured product which increased by 1.9% over the period and had by far the lowest volatility at only 8.1%. This is due to the fact that principal protected products cap losses (in this case up to 5% of the investment) and therefore market falls have a smaller effect on these than on at risk products. Principal protected products are in general neutral or long volatility so increases in volatility caused by short term market decline will not negatively affect its value.

Product 2 is a 10 year phoenix autocall linked to Total stock and has the highest volatility and suffered the largest loss. Over the same period Total itself fell by 28%, significantly more than the structured product, which was only down 20%. This product has behaviour that can be observed in all three of the capital at risk products during March, the most volatile period of 2020.

There were significant losses recorded across the market in March 2020, seen clearest by examining the performance of the iShares Core Euro Stoxx 50 ETF. Since most structured products are linked to equities and are “long” the market to some degree (this applies to all four products and the MPS) we would expect major market losses to translate into secondary market price falls and indeed this is demonstrated with our examples here.

The Hilbert MPS has a slightly higher volatility than the ETF over last year. However, its return is significantly higher than the benchmark and it is in fact the best performing of our set. The Sharpe ratio is less than for the protected structured product because the MPS has much higher volatility.

Individual structured products tend to have a delta to their underlyings of less than one which would imply that the price should move by less than the fall (or rise) in the underlying. However, when there are big falls in the underlying volatility generally also increases and for at risk products an increase in volatility usually means a fall in price. Therefore as is happening with our products here the combination of the reference asset decline and increase of volatility can actually lead to a larger price drop for the product than the asset itself. This means that in such circumstances products can fall faster than the market which can be unintuitive and unsettling for investors. Later in the year (and into 2021) both markets and volatility moved to improve the secondary market value of these products. There is also a valid argument that short term volatility moves do not penalise long term investors provided barrier levels are not breached.

Last year was a turbulent year for most asset classes and structured products were no exception. An examination of secondary market prices gives insight into how market performance affects product pricing and the value of structured products in a portfolio. However, ultimately these products are still designed as buy to hold investments and in the case of our examples still all have over eight years left to run, giving plenty of time to recover to generate returns for their investors.

Tags: Structured Edge ValuationsA version of this article has also appeared on www.structuredretailproducts.com

Image courtesy of: Rodrigo Kugnharski / unsplash.com