Increasing yield through variation in risk

Structured product plan manager IDAD have started 2021 by bringing an innovative variation on the standard kickout product to the UK market. This product is issued by Societe Generale and the concept was created and developed by the bank who are well known for their innovation capabilities and track record.

The upside generating element of the FTSE 100 Kick Out Plan - Issue 1 follows a familiar autocall structure and has a typical schedule of payments which will be paid if the underlying, (the FTSE 100 Index) is above its initial level on any observation date.

Daily accrual mechanism

The twist in the product relates to the downside risk and the calculation of the amount of capital returned in the case of a barrier breach. If the index is below 65% of its initial level at maturity, the investor will lose some of their capital investment. The amount of capital lost will depend on the number of days during the product term that the index has been below this barrier level. For each trading day that the closing level of the index is below the barrier, 0.1% of capital will be lost. If for example the barrier was breached at maturity and during the product term the index had been below the trigger level for six months, or approximately 126 trading days, then 12.6% of capital would be lost.

The barrier level of 65% is typical of a European barrier level currently seen in the UK although it is higher than has been seen historically due to the relatively unfavorable pricing conditions. It is these same conditions that have driven the need for this new payoff. Persistent low interest rates and reduced dividend levels make it hard to generate attractive headline rates for popular structures like autocall and phoenix autocall products. Investors are used to seeing returns offered at a certain level and when pricing parameters move against structuring these products it is difficult to market the same products with lower returns because there will not be sufficient demand. Generally this is when we see products moving somewhat up the risk scale in order to keep the level of returns consistent. The key is to do this in a managed and transparent way.

Once it has been decided that more risk should be introduced in order to offer higher returns providers have a few options to consider. A common choice is the introduction of one or more additional underlying assets on a “worst-of” basis which will increase the probability of capital loss. It also introduces complexity and correlation risk into the product. Another mechanism available to providers is to swap out the popular FTSE-100 index with a different underlying. The current trend is to keep a UK focus but use an asset with a dividend mechanism which makes pricing more favorable and therefore a higher return can be achieved.

Variation on single index product design

The product here has avoided both of these variations and been developed as another way to generate higher returns whilst keeping much of the same product structure.

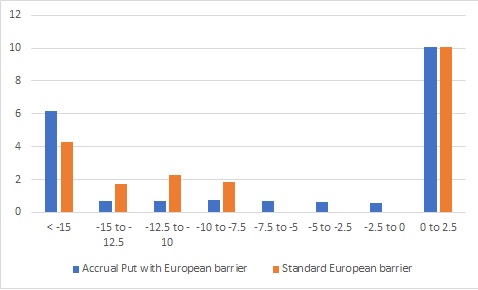

The graph shows the simulated probabilities of the IDAD downside accrual barrier and an otherwise identical product with a standard European barrier of 65%. (Source: FVC Structured Edge.) Firstly, this shows that the probability of not breaching the barrier is the same as would be expected. In both cases the final level of the index needs to be below 65% for the downside to knock in. The total probability of loss is also the same in both cases, 10.15%. The difference between the outcomes of the two barriers can be seen in the more granular breakdown where it becomes clear that the new accrual barrier has higher chances of larger losses.

According to the same simulation results the accrual barrier has a 1.24% chance of returning zero capital at maturity. This would happen if the index was below the required level for 4 years out of the 5 year product term and finished below 65% of its initial level. For a typical European barrier the probability of a zero return is negligible as it would require the index itself to fall to zero.

Positioning for different market scenarios

This accrual feature has been developed as a way of generating higher returns by introducing more risk. Since the chance of loss is the same it should come as no surprise that the magnitude of losses are expected to be higher. However, the 10 year backtesting results for both downside variations show no cases where the investor had lost capital showing that this strategy has performed well historically.

The rationale for offering this kind of structure is that although this product would perform poorly in a bear market it would only perform worse than a standard European barrier if the bear market was sustained for a sustained period which is historically has not been seen very often. Comparing this product with a standard barrier product it would only perform worse than if the index was below the 65% barrier (4310 index points at todays level of the FTSE-100) for at least 1.6 years out of the 5 year product term. Any less than this then the product would outperform the standard structure. If the index recovered to over 65% at maturity then both types would pay full capital.

This product is a good example of how structured products are able to adapt to market conditions and develop features that align with investors risk appetite. The product has the same trigger level for capital loss as many FTSE linked products available on the market so the investor has to determine whether the potential for greater losses if this occurs are worth the additional upside potential.

Tags: Structured EdgeA version of this article has also appeared on www.structuredretailproducts.com

Image courtesy of: Laura Ockel / unsplash.com